• 5 MIN READ

A Full Overview of VAT Codes: Every Code Explained

March 26, 2024

What Is VAT?

Value-added tax (VAT) is a critical component in business transactions and consumer pricing. It is an indirect tax, an extra charge on the price of a product, levied at every stage of the supply chain where value is added. For businesses, knowing the VAT registration threshold, VAT filing deadlines, and other VAT-related specifics is essential to legal compliance.

In this article, we’ll focus on the meaning of VAT and look into VAT codes and rates. You will also learn about methods to keep VAT records and simplify tax reporting using modern software like Payrow. Let’s dive in.

What Does Value-Added Tax Mean in the UK?

VAT is a tax that is included in the price of a good or service throughout the entire chain of production and distribution, from raw materials to the retail sale of finished goods. VAT raises substantial revenue, making it an attractive option for the UK government. Moreover, value-added tax can help the country address fiscal issues and accelerate economic recovery.

VAT is levied in stages, allowing only the value added at each stage of the supply chain to be charged. This system helps to avoid double taxation and ensures transparency of tax payments. VAT rates vary from country to country. Some sales of goods and services are outside the scope of VAT. This means that the value-added tax doesn’t apply to them. Now, let’s move on to HMRC VAT rates.

Standard VAT rate

The standard VAT rate in the UK is 20%, applying to most goods and services. The standard rate provides a stable income for the government, making a significant contribution to the public finances along with income tax and National Insurance.

Reduced VAT rate

There is also a reduced rate of 5% for specific items like some health products, fuel, heating, and car seats for children. The reduced rate is necessary to provide relief and support to businesses, stimulate economic activity, and help businesses recover from financial distress by reducing the cost of the goods and services they sell to consumers.

Zero-Rated VAT Items

A business must charge the standard rate unless its goods or services fall into the VAT categories with the reduced or zero rate. Zero-rated VAT products include most food and children’s clothes, books, and newspapers. VAT on digital services is 20%, with some exceptions — certain publications may qualify for a zero rate of VAT. VAT relief schemes such as the zero rate are necessary to make essential goods more affordable to consumers. With a 0% rate, businesses can recover VAT on purchases.

VAT Exempt Goods and Services

VAT exemption means that goods and services are not subject to VAT, and businesses cannot recover VAT on the costs associated with them. VAT-exempt goods and services are insurance, financial services, investments, education, and medical treatment. Businesses selling VAT-exempt goods cannot register as VAT taxpayers if their sales are exclusively VAT-exempt and they are not eligible for the VAT reclaim process.

Read more: Zero VAT and VAT Exempt – What’s the Difference?

The Difference Between VAT and Other Taxes

The main difference between value-added tax and other taxes is how it is applied and levied. VAT is charged at every stage of the supply chain — from suppliers to manufacturers, distributors, retailers, and finally, consumers. All sellers charge VAT, and all buyers pay it on their purchases. Businesses track and document the VAT to receive a credit on their tax returns.

In contrast, income tax is levied on various types of income and is deducted from income under the PAYE system, where employers deduct tax before paying employees’ wages. The rates of tax depend on the employee’s level of income. National Insurance is a deduction from earned income paid by those over 16 and under pension age. It funds state benefits such as the Employment and Support Allowance and Retirement Pension.

Read more: Taxes in the UK: The Difference Between VAT and Tax Returns

How VAT Works

VAT-registered businesses are legally obligated to charge VAT on the goods they provide, report the amount they charge via a VAT Return, usually completed every quarter, and pay the VAT they have charged to HMRC. The VAT registration threshold in the UK for 2024 is set to increase from £85,000 to £90,000. This change will come into force on the 1st of April, 2024. This means that any business that has an annual taxable turnover above this limit is required to register for VAT.

VAT-registered businesses collect VAT on behalf of the government and pay it at regular intervals, depending on the scheme used. Each business must be aware of the exact payment schedule and the applicable rates.

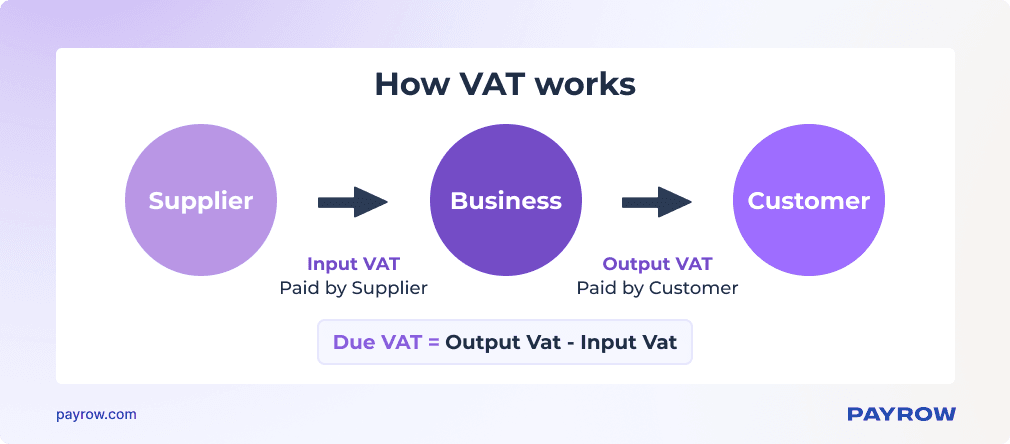

A business charges an output tax to customers and pays an input tax to suppliers. The difference between the two is either paid to or reclaimed from HM Revenue and Customs. In the graphic, you can see the comparison of input VAT vs output VAT.

If you have charged more VAT than you have paid, you must pay the difference to HMRC. If you have paid more VAT than you have charged, HMRC will refund you the difference. Also, there are VAT schemes that affect how a business calculates and reports the VAT it owes to HMRC.

In the UK, import VAT is levied on goods imported into the country from another nation. It is typically charged in addition to customs duty. The rate is commonly around 20%. Export VAT is applied to goods and services sold outside the country. Most of them are eligible for zero-rating.

VAT Codes Explained

A VAT code demonstrates the tax rate applicable to goods and services in the UK and helps to determine the correct amount of VAT payable on different transactions. VAT tax codes also play an important role in categorising business activities.

If a business owner understands and applies correct VAT codes, the chance to ensure accurate tax compliance and avoid penalties increases. These codes not only help businesses follow HMRC regulations but also assist in understanding official documents where they may be present.

Commonly Used UK VAT Codes

HMRC VAT codes are alphanumeric and are used to determine the amount of value-added tax due. Here is a VAT codes list for the UK.

- VAT Code S refers to the standard rate, which is set at 20%.

- VAT Code R refers to the reduced rate, which is 5%.

- VAT Code Z denotes zero rate, a rate of 0%.

- VAT Exempt or N/A represents VAT-exempt goods and services that are not taxable.

HMRC also uses reverse-charge codes for specific cases. With the reverse-charge VAT mechanism, the responsibility for accounting for VAT shifts from the supplier to the buyer. These are:

- RC SG — Reverse Charge Standard Goods, default reverse-charge VAT for services.

- RC MPCCs — Reverse Charge Mobile Phones and Computers, reverse-charge for buying mobile phones and computer chips.

- RC CIS — Reverse Charge Construction Industry Scheme, reverse-charge VAT code applicable to companies operating within the construction industry scheme.

Other codes commonly used in the UK are sage VAT classifications. The sage VAT codes list includes:

- T0 — zero-rated transactions

- T1 — standard rated transactions (20%)

- T2 — exempt transactions (0%)

- T5 — reduced rate transactions (5%)

- T9 — transactions featuring non-vatable items

- T20 — transactions subject to VAT reverse charges

Lastly, there are VAT codes on Morrisons receipts, which do not look like standard codes but are often used. Here’s what they look like:

- VAT Code A — 20% VAT

- VAT Code C — 10% VAT, a blended rate for children’s items

- VAT Code D — 0% VAT

- VAT Code F — 0% VAT

Morrisons receipt VAT code F and VAT code D both represent zero-rated items and mean that the product bought is non-taxable. Two codes may be used for different types of items or internal reporting purposes at Morrisons.

Identifiers used for value-added tax purposes in the European Union are called the EU VAT codes. There’s a separate VAT code list and unique VAT number format for each EU country.

How to Keep VAT Records

Regardless of whether you pay VAT or only sell VAT-exempt goods, you need to keep records. Just as you keep track of the supply chain for your business, you need to keep track of VAT. This is necessary to comply with tax regulations or VAT invoice requirements and fill in a VAT Return.

Maintain Detailed Records

Keeping comprehensive records is essential. A business should have full and accurate records for at least six years (if possible), including invoices, receipts, and summaries of VAT charged and paid. Maintaining records could be very helpful in case of VAT compliance checks. It’s important to note that the systematic recording of VAT transactions involves adherence to specific guidelines and legal requirements to ensure accurate documentation. These can be found in the VAT guide.

Organise Your Records

To avoid getting tangled up in the documents that you’ll be collecting for many years, it’s better to store them all digitally. Many people choose to organise them in a spreadsheet format such as Excel. However, given how quickly technologies develop, this format is already obsolete, so you may opt for highly specialised software and industry-specific digital solutions for tracking taxes. You can use Payrow for such purposes, as it eliminates paperwork and automates document management.

Monitor Your VAT Account

Once everything is set up and you are collecting and paying VAT correctly, it is important to monitor VAT payments and refunds and keep proper records for tax audits. This requires monitoring to help identify any discrepancies or errors in VAT calculations. You may need to make VAT adjustments, correct errors in VAT returns, and ensure that you are paying the right amount of VAT. Monitoring also gives you a clear picture of your liabilities, which is essential for better financial planning.

Payrow Services for Tax Management

Now that you know about dealing with VAT, you may be wondering how to make it easier. Today, there are digital solutions that help not only with tax management but also financial planning, invoicing, and data monitoring.

The Payrow platform was designed to help startups, SMEs, freelancers, and businesses in the HoReCa segment. The features of the platform include:

- UK and international business payments

- Automatic invoicing and statements

- Transaction scheduler

- Smart expenses control

- and much more

At Payrow, you’ll find accounting management software instruments, as well as guides and news for compliance and administration. Streamline the tax management processes and make accounting easier with user-friendly Payrow tools.

FAQ

What are the current VAT rates set by HMRC?

The UK VAT rates in 2024 include the standard rate of 20%, the reduced rate of 5%, and the zero rate of 0%. There are also VAT-exempt goods and services. The rate depends on the items your business buys and sells.

What are VAT codes?

VAT codes are alphanumeric codes used to denote the percentage of value-added tax. Each VAT code in the UK helps to determine the amount of VAT payable on different goods and services. There are standard HMRC VAT codes, reverse-charge codes, sage VAT codes, and VAT codes on Morrisons receipts.

How do VAT codes in the UK aid in categorising transactions for tax purposes?

When you document the amount of VAT you have charged or paid, you need to specify the category of items to which it is applied. This will be much easier to do if you use VAT codes. Instead of writing “reverse-charge VAT for buying mobile phones and computers”, you would just write “RC MPCCs”.