• 5 MIN READ

Zero VAT and VAT Exempt – What’s the Difference?

April 12, 2023

As in many other jurisdictions, taxes in the UK are not the same for everyone. As a business owner, you need to understand which taxes may apply to you. One of these taxes is VAT (Value Added Tax). VAT has a fixed rate set by the state; in the UK, it is 20%.

However, this rule does not apply to all products. There are also some goods and services, for example, children’s car seats and home energy, on which the VAT rate is 5%, as well as goods with a zero rate, for example, most food and children’s clothing. Lastly, there are products that are exempt from VAT.

Since VAT is not levied on goods that are exempt from VAT and it is not levied on zero-rate goods, you might think that these terms are interchangeable, but that is not the case. There is a critical difference that you need to understand. In this article, the experts at Payrow explain how VAT works and what the difference between zero VAT and VAT exemption is.

Also, read the article 'Taxes in the UK: The Difference Between VAT and Tax Returns'

What Is VAT and Why Do We Need It?

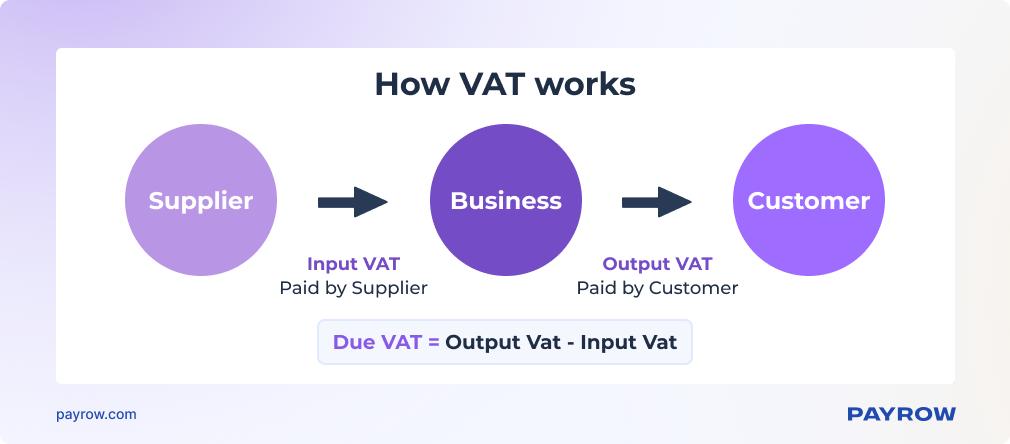

Before we go any further with exemptions and rates, let’s see what VAT means. Value-added tax is a consumption tax applied to goods and services as they move through the supply chain, from the manufacturer/supplier to the business and then to the customer.

VAT-registered businesses collect VAT on behalf of the government and pay it back to them at regular intervals, depending on the scheme they use. Each enterprise should know the exact payment schedule and industry rates that apply. VAT applies to various types of goods and services, regardless of whether they are digital or physical. So, before you even start selling e-books, check the VAT rates.

How Does VAT Work?

Businesses charge an output tax to customers and pay an input tax to suppliers. Businesses registered as VAT payers charge an output tax to customers, which can be compared to sending an invoice, as well as paying an input tax to suppliers, which is like paying an invoice.

The difference between the two is either paid to or reclaimed from HM Revenue and Customs (HMRC) – and this is key here. There are two possible scenarios:

- If a business pays more VAT to suppliers than it charges to its customers, HMRC usually repays the difference.

- If it earns more from customers than it pays to suppliers, then the company must pay the difference to HMRC.

On the issue of VAT, the state is as rational and fair as possible: the main underlying idea is that enterprises pay as much as they collect or reclaim the difference, eventually reaching break-even.

When Does VAT Matter?

VAT is usually included in the listed price, and it’s visible when its rate is 20% or 5%. From the buyer’s perspective, it does not matter much whether the product or service is zero-rated or exempt – there’s no VAT to pay either way. However, it matters to the seller whether VAT incurred on the expenses associated with providing goods or services can be reclaimed by HMRC. And if a major part of the company’s costs has VAT, this can make a huge difference.

If a business sells only VAT-exempt goods, it cannot register for VAT – it is a VAT-exempt business. But if it sells some goods or services that are exempt and others that are not, it must register for VAT if it meets the threshold requirements.

Exempt from VAT: Types and Features

There are two ways a business can be exempt from VAT: when the whole company is exempt and when only some products are exempt. Let’s explore the difference.

Exempt Goods and Services

VAT is not charged on:

- insurance, financial services, investments

- education and training

- healthcare and medical treatment

- funeral plans, burial, or cremation services

- charity events

- garages, parking spaces, and houseboat moorings

- property, land, and buildings

- gambling or lottery tickets

- other goods or services from this list.

These goods are exempt from VAT, so they are not subject to this form of taxation. So, as a business dealing with anything from this list, you don’t include sales of exempt goods or services in your taxable turnover for VAT purposes. And if you buy goods exempt from VAT, no VAT can be reclaimed.

The products subject to exclusion are different from the products with a zero rate. In both cases, VAT is not added to the sale price, but goods or services with a zero rate are subject to VAT – at 0%.

Exempt Businesses

If you sell only those goods and services that are exempt from VAT, then your business is also fully exempt from it. There are two main things to keep in mind:

- You cannot register for VAT.

- You cannot refund any VAT that you have incurred because of your purchases or expenses.

This is different from the requirements and rights you have when you sell zero-rated goods or services. If you sell mostly or only zero-rated products, you can reclaim VAT on any purchases associated with these sales. With zero-rated products, you can also apply for an exemption from VAT registration. If positive, you won’t be able to reclaim any VAT. Check out VAT Notice 700/1 to find out how to register.

Zero-Rated for VAT

Zero-rated goods and services are taxed, but the VAT rate for those goods is 0%. This implies that the customer is not required to pay any value-added tax as the rate is 0%.

Nevertheless, as the delivery is subject to taxation, the supplier can reclaim the VAT paid in connection with the expenses incurred for the delivery. Goods and services that fall under the zero-rate category include almost all food and children’s clothing.

Exempt or Zero-Rated? That Is the Question

The determination of whether goods or services are exempt from VAT or zero-rated depends on the particular nature of the supply and the regulations of the country where you sell them. Various items that are considered necessities (essential goods) are either exempt or zero-rated and hence not subject to VAT.

If you want to check whether your sales qualify as exempt or zero-rated, one possible course of action is to refer to the guidance provided by HMRC.

Is it possible for goods or services to be both zero-rated and exempted from VAT?

No, zero-rated and exempted are two different categories. There is no intersection, and the types of goods and services for each category are published on the GOV.UK website.

There could be confusion, as when there is no VAT charged on the supply of goods/services, it is because the supply is either zero-rated or exempted from VAT. So, sometimes it can be ambiguous.

Payrow Automation Tools for Tax Accounting

It is not always easy for businesses to understand taxation, which is why Payrow creates convenient tools to eliminate paperwork and simplify business process management. The Payrow platform helps enterprises process taxes, create invoices, and handle payments securely. The platform has the latest security features to make sure that all your financial data is safe and protected.

Our financial flow optimisation makes accounting management simple, providing users with a seamless experience. We understand that every business is unique, so we offer essential individual support throughout the entire business cycle. Whether you’re a startup or a medium-sized business, Payrow will be of great help to you.

Simplify tax accounting with Payrow automation tools!

Follow us on our social networks: