• 4 MIN READ

Tax Tips for Small Businesses to Make Filing Easier in 2024. Part II

March 1, 2024

We've already started telling you how to pay business taxes, the amounts due and when they're due, as well as how to avoid common mistakes and simplify your financial management. You can read the first part of the article "Tax Tips for Small Businesses to Make Filing Easier in 2024. Part I".

We continue our discussion on calculating business taxes, preparing for the tax season, dealing with complex tax situations, and other essential matters necessary for small businesses in the UK.

Calculating Business Taxes

As we have already mentioned, incorrectly completed tax returns can lead to problems with the regulatory authorities. So, as a business owner, you need to calculate the taxes you have to pay and, most importantly, do this accurately and correctly.

Strategies for Calculating Small Business Taxes

If you’re wondering how to calculate corporation tax for a small business, and it makes you feel anxious, try not to worry. The process for calculating taxes is simple:

- Learn what taxes you pay

- Find out the tax percentage and what it depends on

- Review tax forms and instructions

- Gather income and expense documents

- Find out how much profit your business has for the tax period

- Deduct allowable expenses

- Apply the relevant rate

- Double-check all calculations

- Check that you submit everything in the right period (before the deadline)

- Consult experts and ask for tax advice for startups if necessary

Use everything that can help you — consultations, spreadsheets, business tax software, and even communication with regulatory authorities. They can recommend the top tax planning strategies for entrepreneurs.

Business Expenses: What Can Be Deducted?

Looking back at the process detailed above, in step four, we mentioned the allowable expenses. But what exactly are these, and how do you find them? The most common tax deductions for businesses are:

- Automobile expenses

- Depreciation

- Home office

- Employee compensation

- Bad-debt

- Insurance

- Interest

- Educational expenses

- Pension plans

The list can be continued. The main point here is that you may take steps to claim all the deductions you are entitled to while complying with HMRC tax obligations.

Capital Allowances for Small Enterprises

Capital allowances refer to tax benefits you can claim on the cost of a number of capital expenditures. This means that a business has an opportunity to deduct part of the value of qualifying assets from its profits before paying tax.

Not all assets are eligible for capital allowances, so you need to be careful. Learn about different types of allowances to save as much as you can while staying compliant with regulations.

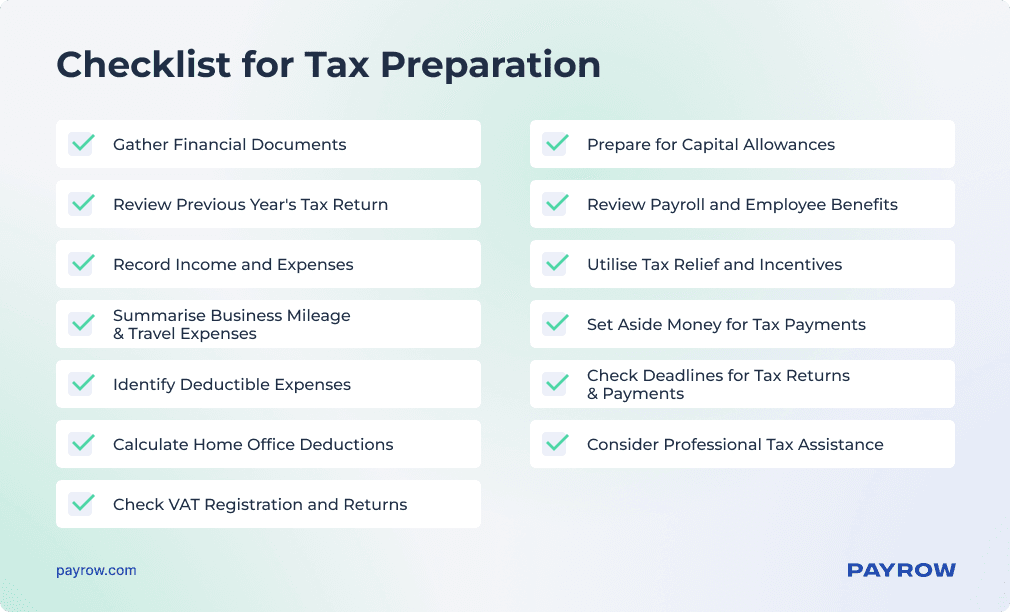

Checklist for Tax Preparation

You don’t need to memorise the entire process and start from scratch every year. Let’s clarify what data you need to have to pay taxes successfully:

Dealing with Complex Tax Situations

Tax payment difficulties can arise if your company has a complex ownership structure, if you missed some deadlines, or if you did not file your VAT business registration application on time. In extreme cases, problems can arise because you don’t have the funds to pay your taxes. What is important to know about difficult situations is that they are all solvable.

How to Handle Uncommon Tax Scenarios

If there are new regulations or you face new taxes, consult with your accountants to define your new scope of tax obligations. Read tax articles on credible websites, watch up-to-date tutorials, learn from the experience of other companies, or seek professional help. UK business tax experts, lawyers, accountants, and even representatives of the regulatory authorities will come to your aid. In addition, tax charities can provide free, confidential advice.

When to Seek Professional Tax Help

Whether it’s paid or free, getting help is never a bad thing. But you may be wondering whether you should always ask for help or whether it’s better to figure things out on your own. Consider consulting a tax expert when you:

- Have just started a business

- Are confused about your obligations

- Don’t know what benefits and credits are available to you

- Don’t know how to use software to store or automate your tax records

- Cannot send data to HMRC for any reason

- Are facing tax disputes with HMRC

Tax Laws and Policy Updates

British tax law is not static, if not to say that it’s constantly changing. Therefore, you are bound to find that tax rates change, reporting forms are frequently revised, new tax credits are introduced, or requirements are tightened. The digitalisation of the economy only accelerates and complicates this process. It’s something you have to be prepared for.

This Year’s Tax Law Changes

Let’s have a look at how the UK tax laws changed in 2023 and what to expect in 2024.

- The main rate of corporation tax increased from 19% to 25% from the 1st of April 2023;

- The thresholds at which employees start to pay student loans for Plans 1 and 4 have increased;

- The National Living Wage is set to increase in 2024;

- From April 2024, employers can pay employees for any given period at a rate of 12.07%. For zero-hours or part-time workers, holiday pay is now legal.

- HMRC now demands e-commerce platforms to report user earnings;

- From April 2024, Class 2 National Insurance, which contributes to state pension credits, will be abolished for the self-employed.

- The tax-free dividend will be reduced from £1,000 to £500 per shareholder in 2024.

- From 2024, the government will abolish the lifetime allowance in pension tax legislation.

Adapting to Changes in Tax Policy

To update their tax strategy for the coming year, companies should regularly study information on this topic, stay abreast of news and adopted laws, follow speeches by government officials, and consult with experts. They can also greatly benefit from Payrow. This FinTech company, with its personalised support and various customisation options, aligns well with the evolving needs of firms facing new tax regulations.

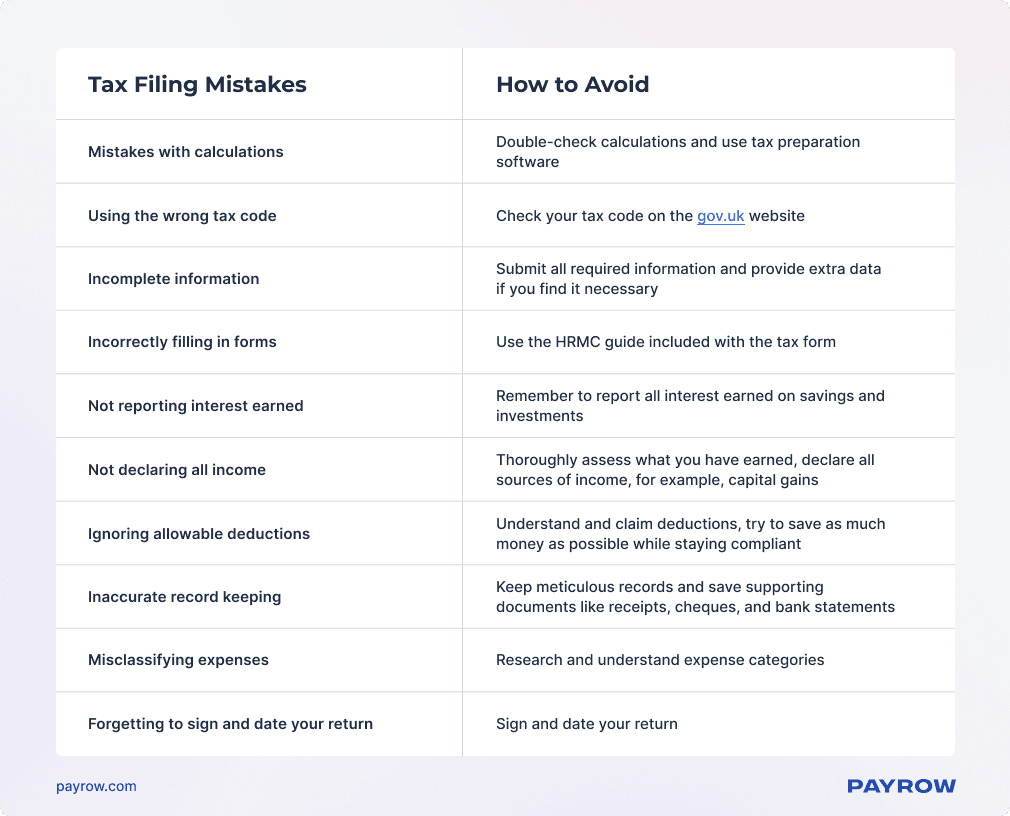

Typical Tax Filing Mistakes and How to Avoid Them

The most common tax filing errors businesses encounter are errors in calculation, choosing the incorrect filing status, missing out on tax deductions, or entering the wrong account number. We have compiled a table of frequent mistakes and ways to avoid them.

Organising Financial Documents

So that you don’t have to worry about missing documents for reporting, the best practice is to organise all of them into a single system. Systematising and classifying files, as well as automatically uploading all financial documents to one place, can make tax preparation much easier. Payrow stands out among the top UK systems for managing financial flows, statements, and invoices. Protected by advanced protocols, the platform can be your best assistant in business process automation.

FAQ

When Are the Key Tax Filing Deadlines for Small Business Tax Returns in the UK?

Here are some key dates and tax filing deadlines for UK businesses:

- The tax year: from the 6th of April to the 5th of April of the following year.

- Corporate tax: nine months and one day after the end of your accounting period. Filing the tax return: 12 months after the end of the accounting period.

- A Self Assessment paper tax return must be filed by the 31st of October. The deadline for paying taxes for business owners is the 31st of January the following year.

How Can Small Businesses in the UK Claim Capital Allowances on Their Tax Returns?

One has to keep in mind that not all assets are eligible for capital allowances. Firstly, you need to check whether your assets qualify for capital allowance. Secondly, support your claim by providing detailed records of the assets you are claiming. Lastly, include a separate capital allowance calculation in your Company Tax Return or on your Self Assessment tax return.