• 6 MIN READ

Revenue vs Turnover in the UK: Breaking Down the Basics

March 18, 2024

An entrepreneur who is just learning basic business concepts may be confused about economic terms. To help you figure them out and manage your company’s budget efficiently, we’ve compared some of the most frequently confused terms — revenue and turnover — and explained the difference between them.

In this guide, you can learn formulas for calculating turnover/revenue, UK taxation peculiarities, and legal considerations, as well as typical pitfalls and best practices for money management. Learn how to assess and improve your company’s performance and business financial health with Payrow.

Defining Revenue in the UK Business Landscape

Revenue is all the money earned from sales, interest, dividends, and rental income over a certain period (a month, a quarter, or a year). It represents the total income a company generates from various activities and does not account for expenses.

Revenue is the top-line figure on an income statement and a key indicator of profitability. It demonstrates the market value delivered to customers, demand for offerings, growth potential, and market share, which makes it one of the most important metrics for businesses. In addition, revenue is often used in economic analysis to determine different profitability ratios, profit margins, and acceptable leverage, as well as for forecasting and modelling.

Revenue may be confused with profit, but they are not the same thing. To create one unit of the product, a company needs to purchase equipment and materials and pay employees and taxes. If you subtract all these expenses from the revenue, you will get a company’s profit.

Revenue Recognition Principles in the UK

The revenue recognition principle states that revenue should be recognised and recorded when it is realised or realisable and when it is earned. In other words, companies should not wait until the cash is actually collected to put it in the accounting records.

Proper revenue recognition is essential for compliance with accounting standards like the International Financial Reporting Standard (IFRS 15) and UK Generally Accepted Accounting Principles (GAAP).

What Constitutes Turnover for UK Companies?

So, what does turnover mean? Imagine a company that produces and sells certain goods. The turnover is the volume of trade carried out by a company in monetary terms at a given time or the rate at which a company replaces assets. This sounds similar to revenue because both concepts share cash flow, but they have differences.

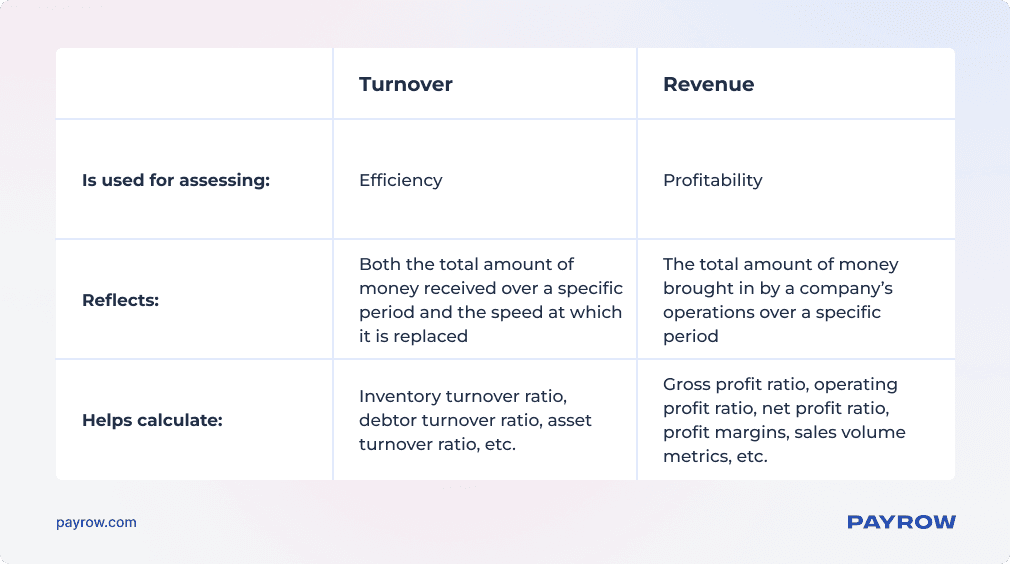

The turnover definition in the UK refers to the total amount of money changing hands within an enterprise. It’s crucial for assessing the company’s resource management efficiency and for planning and controlling production levels. The same term refers to the speed at which a company replaces assets (money, inventory, or investments) and represents the rate of the company in collecting cash and selling products to customers. In business analysis, turnover data is used to calculate debtor, inventory, accounts receivable/payable, asset, and other financial turnover ratios.

Is Turnover the Same as Sales or Revenue?

Turnover and sales are related, but they are not exactly the same. Sales volume is the total number of units sold in a certain time. Turnover, in contrast, reflects the money earned from trading these goods.

When comparing turnover vs income (revenue), it’s important to note that while turnover indicates a company’s ability to generate sales and be efficient, a company’s revenue reflects profitability after expenses are considered.

Are Revenue and Turnover Taxed Differently in the UK?

In the UK, revenue generated by businesses is subject to taxation. It is a key component in determining a company’s tax liability. HM Revenue & Customs is responsible for the administration and collection of taxes. HMRC oversees the taxation process and ensures that businesses comply with tax regulations by reporting their revenue accurately.

Turnover is one of the main factors in determining tax obligations, especially for Value Added Tax. When a business’s taxable turnover exceeds the VAT registration threshold of £85,000 over any rolling 12-month period, it is required to register for VAT. VAT returns are also controlled by HMRC.

So, when answering whether turnover is the same as revenue and is taxed similarly, experts say no. These are two different economic activity measurement tools and are subject to different tax-related procedures.

The Impact of Revenue and Turnover on UK Business Strategy

Being two commonly used metrics, revenue and turnover are crucial for effective business operations and creating a sustainable long-term strategy.

To form a business strategy using these two indicators, a company should develop processes that leverage revenue for growth and profitability and implement measures to optimise turnover for efficient asset use and production management.

It is advisable to regularly monitor revenue and turnover metrics to track performance and then adjust your strategy based on this data to enhance business operations.

Revenue and Turnover: Key Performance Indicators for UK SMEs

In the competitive UK business environment, SMEs are particularly vulnerable to revenue fluctuations. Unlike large companies, SMEs are generally more susceptible to crises due to difficulty in downsizing, weaker financial structures, lower credit ratings, and heavy dependence on loans. When a company’s revenue and turnover decline, it may lead to concerns about defaulting, retaining employees, sustaining supply chains, and even business survival.

Revenue and turnover are KPIs for evaluating the UK SME financial strategies. Monitoring them helps to conduct a financial performance analysis and alter management strategies if needed. One of the most fundamental financial KPIs in the UK that all SMEs should track is sales revenue, as it is used to assess their growth over the years. If you report revenue growth on a regular basis, your business will have a better chance of getting attention and help from investors, as a profitable company is considered more attractive.

Main Types of Turnover and Revenue

You may have seen that income statements don’t always allocate revenue and turnover to only one line for each. This is because each of these metrics is unique.

Revenue can be divided into two main groups, depending on the source.

- Operating revenue is generated from a company’s core activities, which are typically the main source of income. These include product sales, services, licencing, etc.

- Non-operating revenue is generated from activities unrelated to the company’s primary activities, such as income earned from interest, sale of assets, or dividends.

Turnover can be categorised based on various assets and elements within a business’s operations.

- Capital turnover

- Inventory turnover

- Asset (cash, debt) turnover

- Investment turnover

- Customer turnover

- Employee turnover

As opposed to revenue, the term refers exclusively to the turnover of money.

Formulae for Calculating Turnover and Revenue

As we mentioned in a section devoted to the use of these metrics for building business strategies, calculating turnover and revenue is essential for assessing financial performance and operational efficiency. Here are the formulae.

Calculating Turnover

The formula for calculating turnover depends on the specific type of turnover you are interested in. If you need to learn the total amount of money the company makes in a given time period, use this formula:

Total Turnover = Sum of all Sales or Income Generated

Calculating Revenue

Revenue is the total income earned by a company from its operations. Revenue calculation formulas include elements such as sales revenue, service fees, consulting fees, rental income, and other sources of income. The formula for determining revenue varies depending on the specific components that make up a company’s revenue, so each company may have a different formula.

Why Is It Important to Know the Difference Between Turnover vs Revenue?

For business owners, knowing the distinctions between these indicators is essential.

So, turnover is used to ensure financial stability, while revenue is used to ensure the company’s viability in the current business environment. In addition, there are different considerations for revenue and turnover for UK companies in terms of taxation.

Legal and Tax Considerations in the UK

Following the business revenue law in the UK, companies are subject to Corporation Tax on their profits, which can be determined by subtracting total costs from total revenue. If the wrong value is used to calculate profits, there could be tax payment issues (overpayments or debts) and potential disputes with HMRC.

Every company in the UK is obliged to pay taxes correctly and on time; otherwise, it will be prosecuted. There are also UK annual sales reporting requirements, tax audit procedures, financial reporting standards, and common accounting practices for the UK.

Revenue and Turnover Reporting Obligations for UK Entities

UK companies have specific reporting obligations based on their turnover, revenue, assets, and number of employees. They are primarily governed by the Companies Act 2006 and other relevant regulations.

Private limited companies (LTDs) must file statutory accounts at Companies House. In the Companies House accounts guidance, you can read more about accounting reference dates (ARDs), record-keeping rules, preparing accounts for each financial year, exemptions, deadlines, and penalties.

Additionally, large companies and trusts are subject to sustainability reporting requirements like the Streamlined Energy and Carbon Reporting (SECR) policy.

Best Practices for Managing Revenue and Turnover in the UK

The best practices for dealing with revenue and turnover that could be helpful for business operations include:

- Differentiating revenue and turnover, understanding the terms and their use cases;

- Accurately reporting revenue and turnover in financial statements to comply with UK tax regulations and to maximise eligible tax deductions and allowances;

- Using revenue data to plan longer-term business activities and manage resources;

- Using turnover data to manage production levels efficiently;

- Monitoring revenue to calculate profitability and business growth metrics;

- Using both revenue and turnover data to mitigate financial risks.

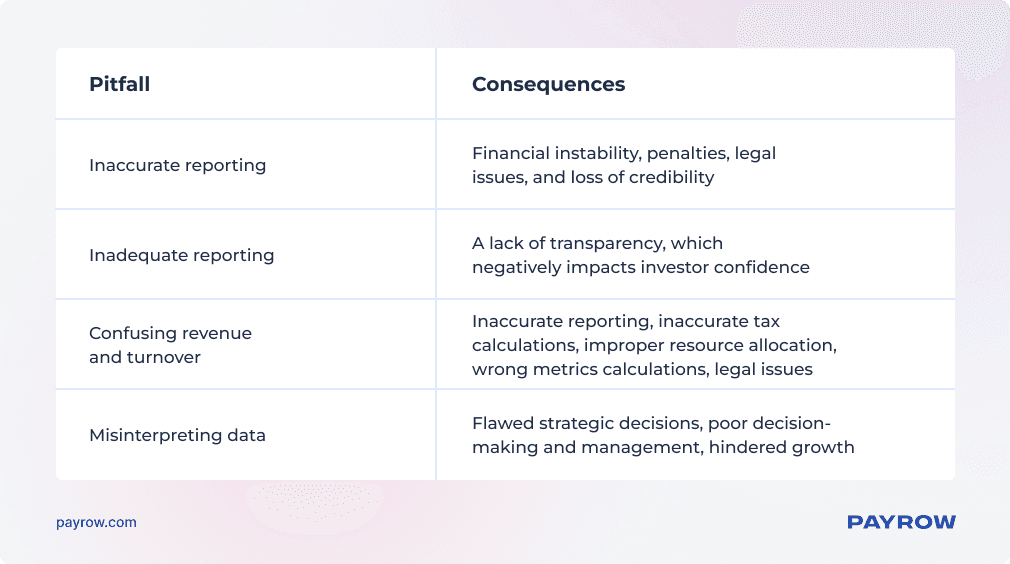

The Pitfalls of Mismanaging Revenue and Turnover in UK Businesses

Entrepreneurs and accountants make common mistakes related to revenue and turnover. To help you avoid these pitfalls, we’ve listed some issues that may arise.

Software Solutions for Tracking Revenue and Turnover in the UK

Businesses in the UK can greatly benefit from various software solutions that help them track revenue streams, turnover, profit, and cash flows. These tools offer features like forecasting, data analysis, pricing optimisation, and automation to streamline revenue management processes.

For example, there is pricing software, banking service providers, AI-powered platforms for retailers, trade promotion management applications, and tools aiding e-commerce businesses in making data-driven pricing decisions. You can find software for almost any business task.

Payrow for Tracking Revenue and Turnover

One of the most powerful tools for money management is the Payrow platform. It offers services for UK small and medium-sized enterprises, e-commerce businesses, the HoReCa segment, and freelancers.

There you can find effective instruments for international business payments, automatic invoicing and statements, automated recognition and receipts, expense management, and much more. Payrow guarantees transparent pricing and no hidden fees. Learn more about our services and contact our experts if you have any questions about the platform.

FAQ

Is revenue the same as turnover?

Revenue, in the context of corporate finance in the UK, refers to the money that a company earns by selling goods and services for a price to its customers. Turnover refers to how many times a company makes or burns through assets, or how much money a company makes in total in a year.

What are revenue recognition principles in the UK?

According to revenue recognition principles, UK businesses must recognise and record their revenue when it is realised or realisable and when it is earned. This means that they don’t need to have cash on hand when the revenue is declared in the company’s financial statements.

In terms of taxation, are there different considerations for revenue and turnover for UK companies?

In the UK, revenue is taxable. Calculating taxable revenue involves determining the portion that is subject to taxation after deductions and exemptions. Turnover, in turn, is not taxable, as it is only a factor in determining tax obligations, especially for Value Added Tax.

How can I use software solutions like Payrow to track and manage revenue and turnover?

As a UK business, you can use the Payrow platform to track money flows, allocate resources, plan business activities, make domestic and international payments, automate accounting and invoicing, and more. Save time with efficient financial management solutions.