• 7 MIN READ

How to Send a Remittance: A Complete Guide

February 27, 2024

People in low-income countries benefit greatly from remittances, which play a significant role in national economies, and they’re an invaluable tool in the battle against poverty. Everything you need to know, right from the meaning of remitted money to the legal complexities involved, is covered in this article.

Understanding Remittances

The remittance definition, in general, is the process of sending money to a third party, either for payment of goods and services or as a gift. A remittance may serve several objectives, such as settling company debts or sending money to loved ones. Many individuals save up while working overseas and then transfer the money to their family members back home. Thus, to many people, the meaning of remittance is the process of sending money abroad.

The Basics of Remittance

Many families in underdeveloped countries rely on remittances as a source of income to cover essentials, including food, education, healthcare, and shelter. Sending money to loved ones abroad has become simple using remittance services, which can be accessed via internet platforms, money transfer operators, or banks. The World Bank migration development brief estimates that remittances to low- and middle-income countries stood at $669 billion in 2023.

Remittances Explained

What does remittance mean? - It is money sent back or transferred to an external entity, such as a company, supplier, employee, friend, family member, or any other organisation. The term “remittance” is most often used to describe money sent abroad.

“For many countries, money transfers from citizens working abroad are a lifeline for development.”– International Monetary Fund

What Does Remittance Mean in Banking?

So, what is a remittance in banking? In this sector, a remittance can be defined as the transmission of funds between parties. As a form of payment or gift, it often entails transferring money from one bank account to another. Electronic payment systems, wire transfers, postal orders, and cheques are all acceptable methods of transmitting remittances to pay bills or invoices. The root of the word “remit”—“to send back”— is where the remittance payment meaning originates.

The Process of Remitting Funds

The majority of remittances nowadays are processed using electronic payment systems offered by banks or money sending services like Payrow. There are three stages to a standard remittance transaction:

- Stage 1 - The sender remits the funds to a money transfer service through a credit/debit card, cash, cheque, online transfer, or money order.

- Stage 2 - The money transfer service delegates the delivery of the remittance to its agent in the beneficiary’s country.

- Stage 3 - The paying agent transfers the funds to the beneficiary.

Types of Remittance Services

Based on the intended recipient and the reason for the transaction, remittances can be either inward or outward. Let’s get to grips with the meaning of remittance types.

- Outward Remittance – Money sent out of one country and into another is known as an outward remittance. These occur when doing business internationally or using services offered by a foreign company. The term also refers to funds sent from people living in one country to family members in another.

- Inward Remittance – In the same vein, these are funds received, often from abroad. This could refer to money received from relatives living overseas or payments for goods and services from international customers.

How Do Remittance Payments Work?

There is a uniform procedure that all transactions must follow to complete the payment cycle. Factors such as availability of bank accounts, currency preferences, speed, and transaction cost influence the choice of payment method. The most common types of payment remittance fall into these major categories:

- Donations

- Health care

- Gifts

- Tuition fees for universities

- Financial assistance

- Expenses related to travel

- Gains from domestic deposits or asset sales

- Financial Investments

The Mechanics of Sending a Remittances

The sender’s bank account must have sufficient funds to cover the transfer before it can be completed. Following the initiation of the transaction, the money will be transferred to the recipient’s bank for further processing. A transaction fee and currency exchange rate are imposed after the funds are received by the bank. After deducting the fees, the receiver can retrieve the cash in their local currency.

Remittance Payment Methods

Sending a remittance payment can be done in several ways. Here are the five common ways to transfer money abroad:

- Cheques - Although cheques are seen as a little quaint for B2C transactions, they are nevertheless widely used for B2B transactions.

- ACH - An ACH is a digital cheque. The process involves pulling funds from one bank account and depositing them into another.

- Credit Cards – Credit cards have been around for a long time. Reliability in payment acceptance is ensured by using these payment methods.

- Bank transfer – Using the conventional wire transfer process, money can be transferred between bank accounts through a “wire.”

- Electronic funds transfer – Digital payments, like an Electronic International funds transfer, are a rapidly growing payment mechanism.

Choosing the Right Remittance Service

Finding a reliable money transfer provider can be difficult; nevertheless, you should not rush into a choice without first doing thorough research and comparing the options available. Finding the best service for your needs is possible if you take the following into account -

- Fees

- Exchange rates

- Speed

- Convenience

- Secure fund transfer

- Customer service

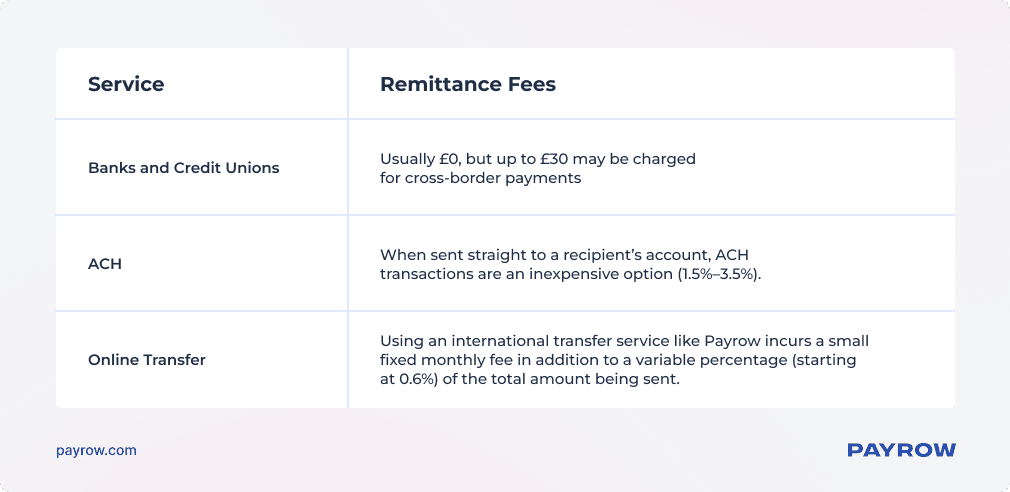

Understanding Remittance Fees

Remittance charges are fees levied by the bank or financial institution initiating the transaction. They generally depend on the amount of money being remitted. The fees fluctuate depending on the charges imposed by the banks.

The Impact of Exchange Rates on Remittances

Remittance flow is drastically boosted by foreign jobs and exchange rates. Decreases in the value of a nation’s currency relative to another’s will attract remitters and may have a positive impact on the amount of money sent to that country.

Conversely, remittances slow down when the recipient country’s currency appreciates. Government initiatives to stabilise a currency rate and encourage formal remittances lead to predictable exchange rates. Remittance receivers can employ financial products like hedging tools to mitigate exchange rate risks while maintaining a consistent local currency flow.

Practical Guide to Sending Remittances

Remittances can be made through bank transfers and other avenues, including third-party services like Payrow. Both the sending and receiving remittance agents work in different countries; the former receives the funds from the sender, while the latter transfers them to the recipient.

Steps for Sending a Remittance

Here’s what you need to do if you want to send money overseas:

- Choose a money transfer service for your financial transaction process.

- After that, you’ll be asked to provide the recipient’s information. You will need the following details: the recipient’s name, address, bank account number, SWIFT code, phone number, and email address.

- Complete the payment. Common ways to pay at online remittance platforms are credit/debit cards, bank transfers, SWIFT, and cash at dedicated service points.

- The beneficiary receives the payment. The money can either be sent to the recipient’s bank account or can be collected in person.

Remittance Address

Commonly referred to as a “remit address,” this is the address to which invoices and cheques can be sent. This address is created solely for transferring money and works just like any other postal address. It is convenient for individuals or companies to have a remittance address to receive payments from abroad. Another option is to use the address of a real bank, otherwise known as a remittance bank account.

What to Consider When Sending Remittances

Besides the definition of remittance and the time it takes, there are a few more factors to consider while sending remittances:

- Transaction Fees – Be sure to understand all the charges associated with the money transfer before you send anything.

- Transfer Limits – Find digital payment systems that let you transfer funds easily and without any unnecessary restrictions.

- Currency exchange rates – Enquire about the current exchange rate before proceeding with the transfer.

- Full Credit – Certain money transfer services will execute the transaction only after deducting their applicable fees. As a consequence, the recipient will be unable to receive the full credit amount. A money transfer technology that promises full credit should be your first choice.

Documentation Required for Remittance

In most cases, documents verifying the particulars of both the sender and the recipient are required:

- Purpose of payment

- Relationship with the sender/receiver

- Personal information (date of birth, address, occupation, and company)

- Identity, citizenship, and current address

- Bank details

- Source of funds

When dealing with businesses, it’s necessary to provide paperwork, including contracts, invoices, transportation papers, identity documents, and accounting records.

Timing and Delivery of Remittance Payments

Bank transfers across international borders normally require 1-2 days to complete; however, they can take longer due to factors such as the financial infrastructure and restrictions of the destination country. An overseas payment system may take longer than expected to complete a transaction due to the following reasons:

- Compliance (preventing fraud)

- Time zone differences

- Different global payment methods and their processing times

- Currency exchange

- Weekends and bank holidays

The British pound, the US dollar, and the Euro, for instance, are usually processed faster than other, less stable currencies.

Regulatory Aspects of Remittances

The Global Remittances Working Group (GRWG) states that regulations regarding remittance services and money transfer services in general must address the following: supervision, financial and operational soundness, consumer protection, compliance, and admission to the market licensing or registration. Below, we will examine two of these factors thoroughly:

Compliance and Legal Considerations for Remittances

The prevention of illicit use of remittance services depends on compliance in banking transactions. To detect and prevent issues, as well as report questionable conduct to the proper authorities, remittance service providers (RSPs) rely on compliance programmes. Money laundering, terrorism funding, and fraud are the most prevalent forms of compliance risk in the remittance sector.

Anti-Money Laundering (AML) Regulations and Remittances

Service providers in the money transfer industry are required to set strong anti-money laundering policies and processes to reduce the associated risks. Several methods exist that RSPs can use to strengthen their banking transfer regulations and compliance positions. Among them are:

- Adopting a risk-based approach to compliance.

- Conducting Enhanced Due Diligence, i.e. gathering and verifying consumer data

- Monitoring transactions for indications of suspicious behaviour and notifying the appropriate authorities.

Payrow and Remittance Payments

Discover the convenience of Payrow for all your international payment needs! Avoid hassle and hidden costs when transferring funds or making payments to businesses in the UK and overseas. Transfer funds across Payrow accounts and set up sub-accounts in GBP and EUR. Find complete information about your SEPA payments and invoices. With Payrow, you can effortlessly manage international payments, set up automatic invoicing, and enjoy top-notch security with just a few clicks.

FAQ

What is ’remittance’ in financial terms?

The remittance meaning in bank or financial terms is simple. It is when money is sent or received from one party to another in exchange for products or services.

What should I look for when choosing cost-effective remittance services?

Transaction cost efficiency, transparency, speed, security, connectivity, preferred currency, and customer service are important aspects to think about when choosing financial remittance solutions.

How can I reduce the fees for remitting money?

Make use of internet money transfer platforms. Online platforms like Payrow often provide better exchange rates and lower transfer costs than big banks, making them a more cost-effective option for a remittance transaction.

What are the legal considerations for sending remittances overseas?

In the UK, there is no legal limit on the amount that can be sent abroad. Individual banks set daily transfer limits anywhere between £50,000 and £100,000. The United Kingdom has stringent Anti-Money Laundering rules. Money transfers to high-risk regions or industries require EDD from payment service providers.