• 4 MIN READ

Changes in Income Tax Thresholds and Payments

May 16, 2023

There are many types of tax in the UK, each with different bands and thresholds, exemptions, rates, and relief schemes. They differ based on the industries you operate in and the products your company produces or sells. Moreover, the structure of the business also affects tax reporting requirements and deadlines. As the topic is too vast, today, we will only cover income tax.

Income tax is the biggest source of revenue for the government. There have been a number of changes to income tax in April 2023. As the cost-of-living crisis is worsening, and the UK could find itself in recession, it is important to know about your liabilities. This can help you take the necessary steps to plan your expenses.

Income Tax Thresholds News

Chancellor of the Exchequer Jeremy Hunt has decided to freeze the income tax Personal Allowance at £12,570 until 2028. Basic rate taxpayers don’t need to pay any tax on income below this level.

The threshold at which the highest earners start paying the maximum tax rate was lowered. This means that the more a person earns, the bigger the proportion of their earnings must be paid as a tax. Thus, more people will fall into the higher tax category, and they will end up paying more tax.

The Office for Budget Responsibility believes freezing the thresholds until 2028 will result in 3.2 million new taxpayers. As an organisation, which independently assesses the government’s economic plans, they conducted a study that found that an additional 2.6 million people would pay a higher tax rate.

Many people moved into paying income tax and into paying higher marginal tax rates due to threshold policy rises, but this is good for the government and the UK economy as a whole. Freezing the thresholds until 2027-28 is expected to collect £25bn more a year than if the thresholds were raised in line with CPI inflation.

What Income Is Taxable?

How much income tax you pay depends on how much of your income is above your Personal Allowance and how much of it falls within each tax band. There’s also untaxable or tax-free income.

The Personal Allowance in the UK remains £12,570, so you pay taxes only if you earn more than this level. You pay income tax to the state on income from employment and self-employment during the tax year. The tax year in the UK is from 6 April to 5 April of the following year.

Additionally, income tax is levied on some state benefits, rental income and income from savings and investments that exceed certain limits. These rules apply in England, Wales, and Northern Ireland. The rules are different in Scotland.

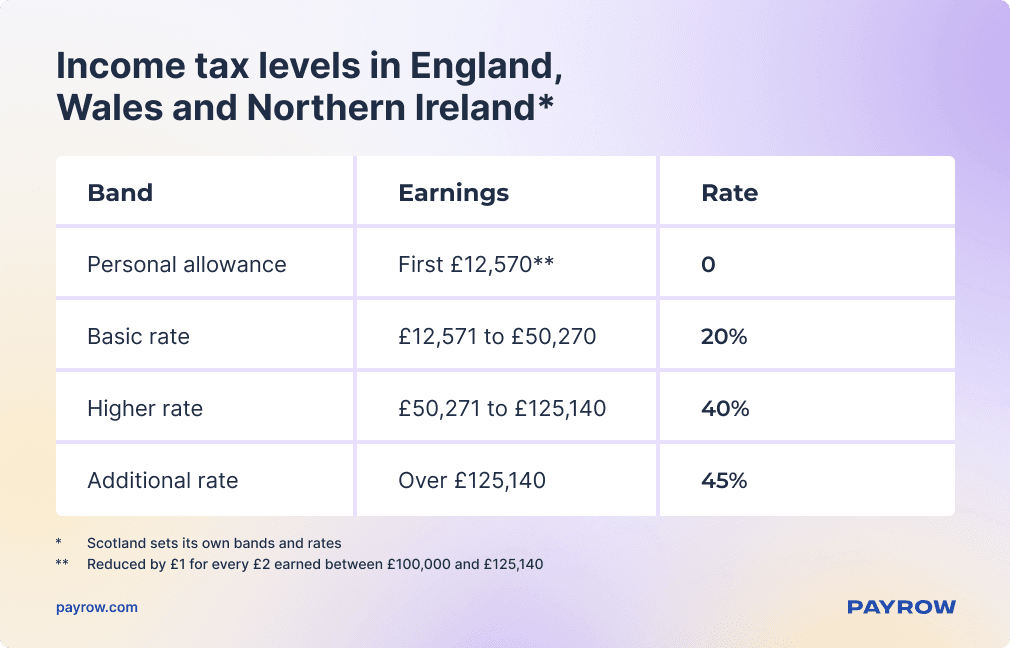

Income Tax Levels in England, Wales & Northern Ireland

UK tax rates are subject to change, so you should find the official information on the government website or check with an accountant. For 2023, the rates in some parts of the UK are as follows. Please note that Scotland sets its own bands and rates.

Personal Allowance amount is reduced by £1 for every £2 earned between £100,000 and £125,140. Below we described each rate in more detail.

What Is the Basic Rate of Income Tax?

The basic rate of income tax is the rate that applies to earnings between £12,571 and £50,270 a year. The UK basic rate of income tax is 20%.

Let’s assume that you have taxable income for the year that equals £40,000. We deduct the Personal Allowance from this amount and get £40,000 - £12,570 = £27,430. In this case, your remaining taxable income falls within the basic rate.

Thus, the tax you’ll pay is calculated this way: £27,430 × 0.20 = £5,486. So, a fifth of the earnings goes to the government in income tax.

What Is the Higher Rate of Income Tax?

The higher rate of tax is called so because it is higher than the basic rate. In the United Kingdom, the higher rate of income tax is 40%. This tax is paid on earnings between £50,271 and £125,140.

Suppose that your income is £60,000, and this exceeds the basic rate upper limit of £50,270. Since it’s £9,730 more than the limit, this particular amount will be subject to a higher rate. To calculate the tax amount, we multiply £9,730 by 0.40 and get £3,892.

When your annual income is over £100,000, your tax-free Personal Allowance decreases, so you need to pay income tax at a rate of 40% on some initial £12,570 earned. The reduction in Personal Allowance is £1 for every £2 of income exceeding £100,000. If your earnings surpass £125,140 annually, you will no longer receive any Personal Allowance.

What Is the Additional Rate of Income Tax?

The additional rate is the 45% tax rate applied to the highest range of taxable income. It’s paid on earnings above £125,140 a year. Before April 2023, this threshold was £150,000, but it has been lowered. According to the government, about 629,000 people pay an additional rate of income tax.

Let’s see an example. Assume that you have earned £200,000 throughout the tax year. Since your income exceeds £100,000, your Personal Allowance is reduced. In this case, the reduction amounts to £50,000, which means your Personal Allowance does not exist any more.

Your taxable income is above the higher rate band of £125,140, which means you should pay a 45% tax on everything above this amount. You subtract £125,140 from £200,000 and then multiply it by 0.45. You will end up paying £33,687 to the government.

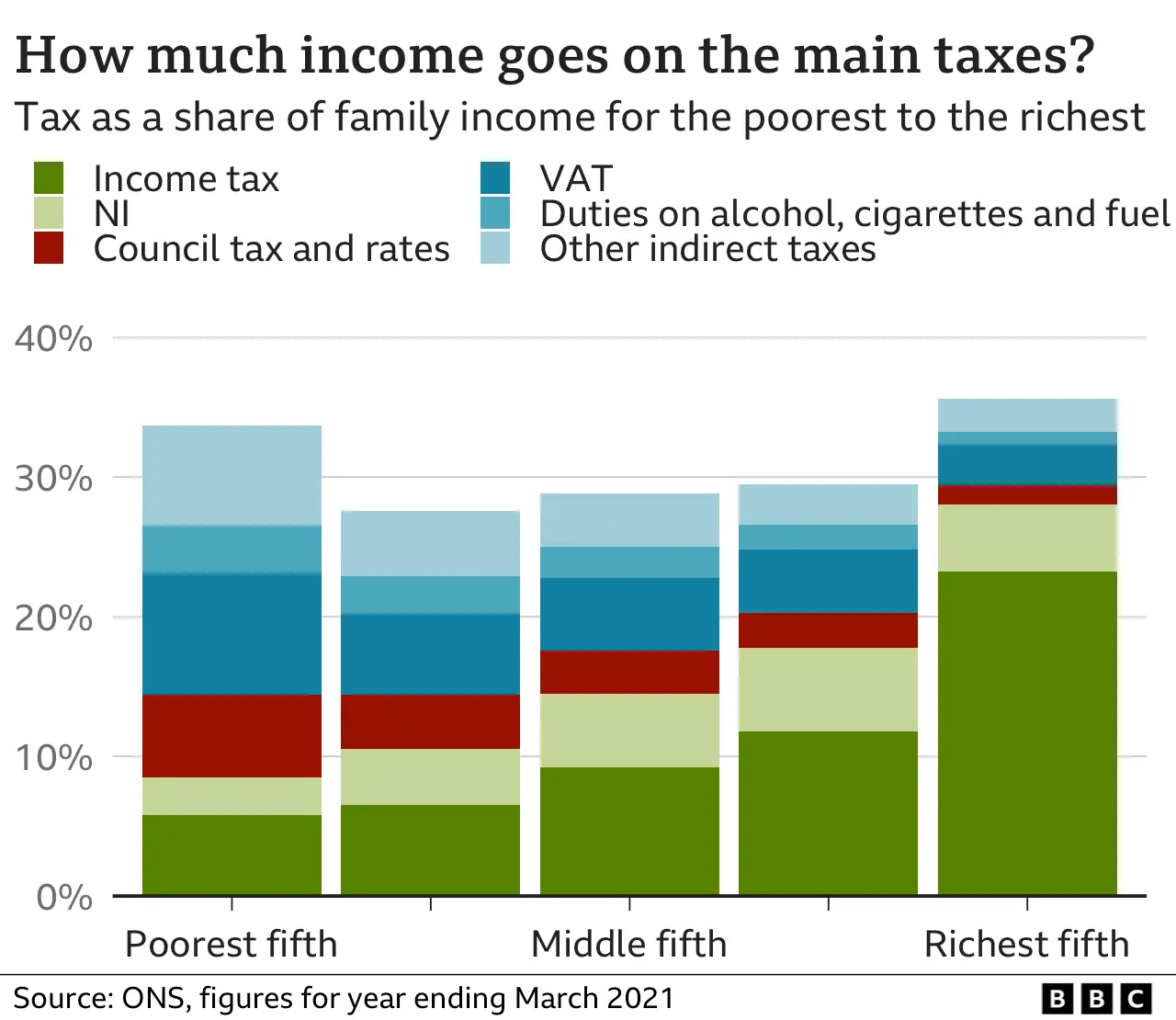

Who Pays Most in Income Tax?

Most families in the UK state that income tax is the biggest tax they pay. Richer people pay more in income tax compared to other households. Poorer families tend to pay a larger share of their taxes through indirect taxes or taxes on expenses like VAT and duties. According to BBC statistics, the poorest fifth of households name VAT as the largest single tax they pay.

{kind=link}

What Is National Insurance?

National Insurance (NI) for employees functions similarly to income tax. It is a fixed percentage of your earnings that the company deducts from your salary. Jeremy Hunt confirmed that the basic National Insurance thresholds would remain frozen until April 2028.

NI is the second-biggest source of income for the government. The scheme has the same thresholds as income tax. To be more precise, annual earnings of £12,571 are not subject to National Insurance contributions. Earnings up to £50,271 are subject to a 12% rate, and earnings above that are taxed at 2%.

The National Insurance Scheme rules are different for people over retirement age. Even if people over the state pension age continue to work, they are exempt from paying NI. In addition, employers are responsible for paying a share of National Insurance contributions.

Payrow Automation Tools for Tax Accounting

Dealing with taxes is a complex and time-consuming process, so many companies use software that simplifies accounting and tax reporting. If you would like to automate routine processes, the Payrow platform is your perfect assistant. Our mission is to help businesses in the UK to grow and develop. We provide startups and SMEs with tools to process orders, create invoices, manage payments, and monitor taxes.

At Payrow, we guarantee that our services have top security measures and that your financial data is safe. Thanks to streamlined financial flow optimisation, managing your accounting becomes simple. To speed up your tax calculation and payment, register on the platform and check out our pricing plans.

Our team of experts is readily available to provide comprehensive individual support at every stage of your business development. Simplify tax accounting with Payrow automation tools!

Follow us on our social media channels: